The individual functions that support credit have always existed. Servicing, portfolio management, and capital markets operations each play an essential role in managing credit.

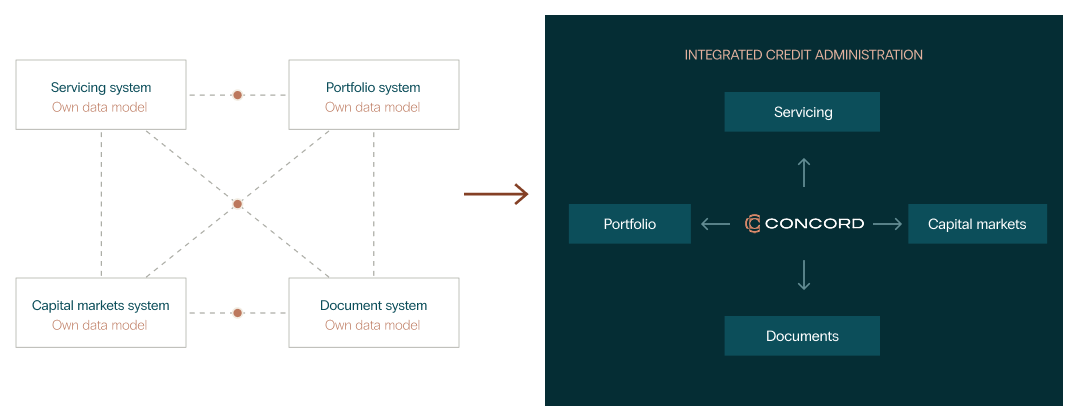

As the industry evolved, each function developed its own systems, teams, and operating models. That specialization improved execution within each area, but it also created separation in how information moved across the credit lifecycle.

Over time, that separation became more visible. Decisions in one part of the lifecycle often rely on information produced in another, but not always in real time or through a shared framework.

The next evolution of credit operations is focused on closing that gap by connecting these functions within a more integrated operating model. One that improves transparency, continuity, and control across the full credit lifecycle.

That model is what the industry is increasingly defining as credit administration.

Credit administration reflects a shift in how the industry structures the work of managing credit. It brings together operational execution, oversight, and supporting infrastructure into a more coordinated system that spans the full lifecycle of a portfolio.

Credit administration organizes how credit is managed across three distinct levels of responsibility:

When servicing data informs portfolio oversight, and portfolio insights connect with capital markets requirements, stakeholders gain a more complete view of credit performance.

For many organizations, credit operations developed in functional silos. Servicing managed loan-level activity. Portfolio teams focused on reporting and performance tracking. Capital markets teams supported financing structures and investor requirements.

The challenge emerges when information needs to move between these functions. That separation shows up in a few consistent ways:

As portfolios grow more complex, coordination between these functions becomes more critical than optimization within any single one. Credit administration addresses this by aligning operational functions around a consistent view of the portfolio.

Credit administration becomes clearer when viewed across the lifecycle of a portfolio. Each stage carries distinct operational requirements, but all depend on accurate information and reliable oversight.

Credit administration begins with the individual account. For consumer portfolios, servicing is where that information is created and maintained. Payment processing, borrower communication, collections, and account maintenance are often viewed as operational responsibilities, but they also establish the accuracy and consistency that stakeholders need.

As Shaun O'Neill, Managing Director of Consumer at Concord, explains:

"The quality of every downstream decision depends on the quality of the servicing data behind it. Credit administration starts with getting the fundamentals right at the account level."

When those activities are executed consistently, portfolios become easier to monitor, report on, transfer, and finance. When inconsistencies develop at the account level, they tend to compound as information moves through the rest of the credit lifecycle

Credit administration begins with disciplined servicing execution because every subsequent layer of portfolio oversight and capital markets administration depends on the integrity of the underlying account data.

Commercial finance portfolios introduce structural and operational variability that increases with scale. Asset types differ, collateral requirements vary, and servicing needs often depend on how portfolios are originated and managed.

The challenge is maintaining clarity across assets that behave differently, particularly when those differences compound at the portfolio level.

As Quentin Cote, Managing Director of Commercial at Concord, explains:

“There’s a fundamental tenet in asset-backed finance (ABF) that enables finance companies to borrow at far lower rates and higher leverage than normal corporate borrowing. The key is the separation of the portfolio of assets from the risk of the originator, both from a performance view and also from a legal perspective.”

That structure only holds when supported by consistent operational execution across servicing, reporting, collateral oversight, and portfolio monitoring.

“If an originator has financial difficulties or another significant change, the servicing quality will suffer," Quentin said.

Commercial finance is not uniform. Bank-owned, independent, and captive models each approach portfolio management differently. But the operational requirement is consistent across all three: visibility, continuity, and the ability to manage assets in a way that is not dependent on the condition of a single organization.

Capital markets administration sits at the intersection of portfolio performance and investor confidence. While servicing explains how an originator manages assets day to day, capital markets administration reflects how those assets are evaluated and trusted over a full investment horizon.

“Servicing proves you can run the asset now; credit administration is what underwrites confidence in the years of performance an investor is actually buying.” — Jeremy Tsui, Managing Director of Capital Markets at Concord

From an investor standpoint, servicing performance establishes execution capability. The focus shifts to whether the operating structure behind the assets can sustain performance across time, scale, and changing market conditions.

As Jeremy explains, "Capital markets administration answers the trust question: Does the investor community have a reason to believe this originator can reliably perform over a five-plus-year investment horizon and adapt across very different macro environments?"

In structured finance, the evaluation extends beyond individual functions. Investors are assessing the durability of the full operating system across origination, servicing, reporting, verification, and custody.

That durability is tested as transactions scale. Most structures now depend on multiple independent parties across diligence, verification, custody, and servicing. Each handoff introduces reconciliation points where data must be revalidated and aligned.

"It's not unusual for a transaction today to involve seven or more parties across diligence, field exams, verification, custody, and servicing. Every handoff is a reconciliation point and a potential point of failure," Jeremy said.

Capital markets administration reduces this fragmentation by preserving consistency of data, documentation, and reporting across the lifecycle, limiting the number of operational seams where breakdowns occur.

As Jeremy frames it, the structural goal is not incremental improvement but reduction in systemic risk introduced through fragmentation:

“Consolidating more of the credit lifecycle under one operating structure meaningfully reduces operational risk, because every seam between providers introduces opportunities for data drift and accountability loss.”

Capital markets administration does not replace functional specialization. It tightens the operating structure around it, improving coherence across the investment lifecycle.

While structure plays an integral role in credit administration, effectiveness at scale depends on systems that maintain consistency across data, documents, and portfolio activity across platforms and stakeholders.

At Concord, our proprietary technology supports each function of the credit administration model:

eVault establishes a verified record of loan and lease documentation through authoritative copy management and a complete chain of custody. It provides structured storage, traceability across document movement, and audit-ready records designed for use across transactions and portfolio lifecycles.

ConcordLink serves as the operational foundation for managing loans, leases, and lines of credit across their lifecycle. It supports payment processing, account management, reporting, borrower communication, and configurable workflows that allow teams to adapt servicing logic across asset types within a single platform.

Finley supports credit facility management, borrowing base automation, covenant tracking, portfolio analytics, and investor reporting. It connects underlying asset performance to the structures that depend on it, improving transparency across capital markets workflows.

The future of credit operations is not defined by individual capabilities alone, but by how those capabilities work together to support the credit lifecycle.

The Hub for Credit Administration reflects Concord’s approach to building that model. Our framework brings together servicing expertise, capital markets administration, institutional processes, and proprietary technology within a unified operating structure.

“One partner, proprietary technology, full lifecycle. That’s what it means to be the hub.” — Dhruv Vakharia, CEO of Concord.

That philosophy prioritizes alignment over consolidation. Each capability remains specialized, but the structure around them reduces separation in how credit is managed over time.

As portfolios become more complex, disconnected workflows create friction in how information is interpreted, validated, and acted on. Over time, that friction reduces visibility and increases uncertainty.

Credit administration provides a framework for aligning how credit is managed across its lifecycle.

At Concord, this operating model is expressed through the Hub for Credit Administration, designed to support lenders and investors with a more connected approach to credit performance, data integrity, and operational continuity.

4343 N. Scottsdale Rd., Ste. 270

Scottsdale, AZ 85251

NMLS ID 365917